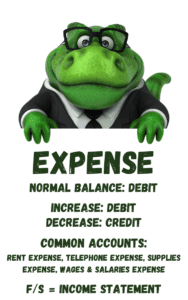

An Expense represents a cost incurred in the making of revenue. Examples of Expenses are Rent, Insurance, cost of goods, and payroll. An expense is also used to record the reduction of value of an Asset. For example, Depreciation Expense is used to record the reduction in value of an Asset like a deliver van. An expense has a normal debit balance. Expenses are listed on the Income Statement.

What are Some Examples of Expenses?

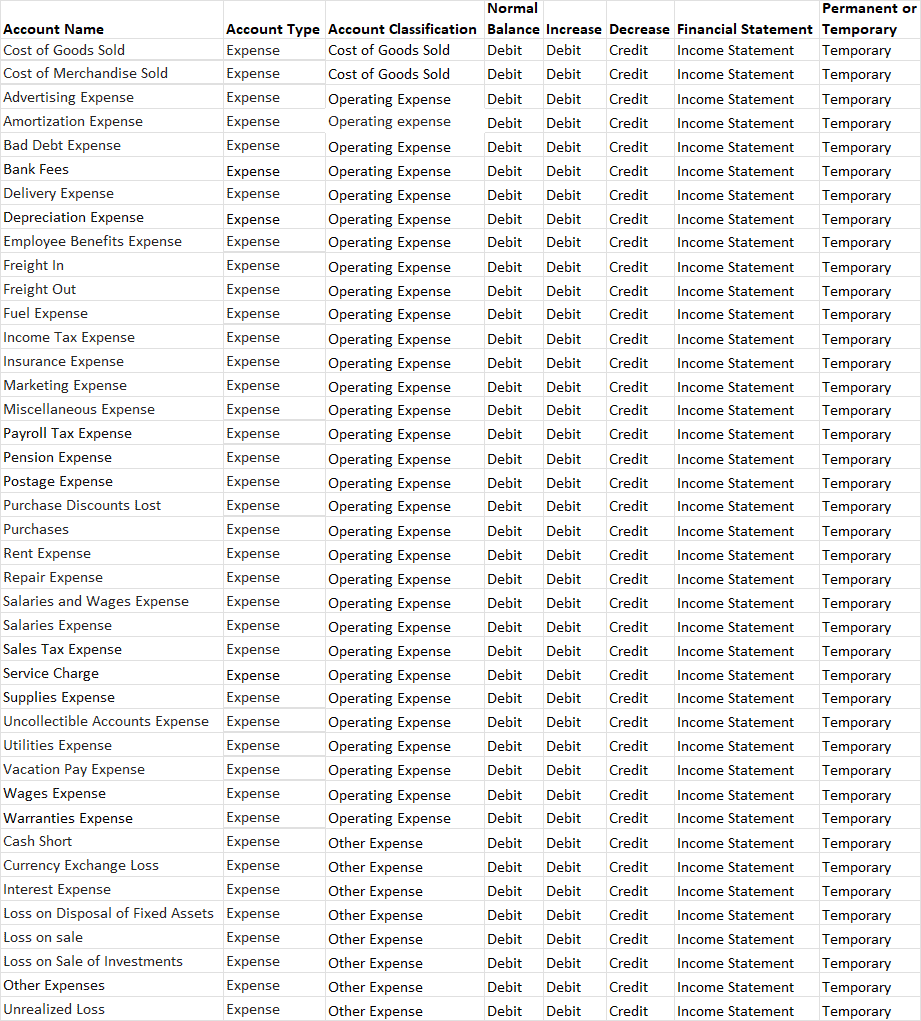

This table shows a list of common expenses businesses use to track the costs associated with creating revenue.

| Rent Expense | Telephone Expense |

| Supplies Expense | Wages & Salaries Expense |

| Delivery Expense | Advertising Expense |

| Commission Expense | Depreciation Expense |

| Amortization Expense | Interest Expense |

| Bad Debt Expense | Payroll Tax Expense |

| Marketing Expense | Utilities Expense |

| Materials Expense | Cost of Goods Sold |

| Cost of Merchandise Sold | Freight in / Freight Out |

| Income Tax Expense | Sales Tax Expense |

What are the Types of Expenses?

Expenses are divided into groups (classifications) depending on their use:

- Operating Expenses

- Non-operating Expenses

Operating Expenses are those costs related to the main activity of the business. Examples of Operating Expenses are Rent Expense, Cost of Goods Sold, and Wages & Salaries Expense.

Non-operating Expenses are those cost not related to the main activity of the business. Examples of Non-operating Expenses may include Interest Expense and expenses from a one-time sale of an assets.

How are Expenses Listed on the Income Statement?

In general, Expenses are grouped together on the Income Statement below the revenue section. The simplest form of the Income Statement, the single-step Income Statement, lists all expense accounts together.

Further classification of Expenses can be done on a multi-step Income Statement. Like Expenses are grouped together. For example, all expenses (cost of goods) related to the making or delivering of a product or service are grouped together. The same can be done with Selling Expenses and Administrative Expenses. Non-operating expenses are grouped together below the Revenue and Expenses from Operations.

Here is an example of a single-step Income Statement:

| Revenue | 10,000 |

| Expenses: | |

| Rent Expense | 1,500 |

| Telephone Expense | 500 |

| Insurance Expense | 1,000 |

| Total Expenses | 3,000 |

| Net Income | 7,000 |

Here is an example of a multi-step Income Statement

| Revenue | 10,000 |

| Cost of Goods Sold | 5,000 |

| Gross Profit | 5,000 |

| Expenses: | |

| Rent Expense | 1,500 |

| Telephone Expense | 500 |

| Insurance Expense | 1,000 |

| Total Expenses | 3,000 |

| Net Income | 2,000 |

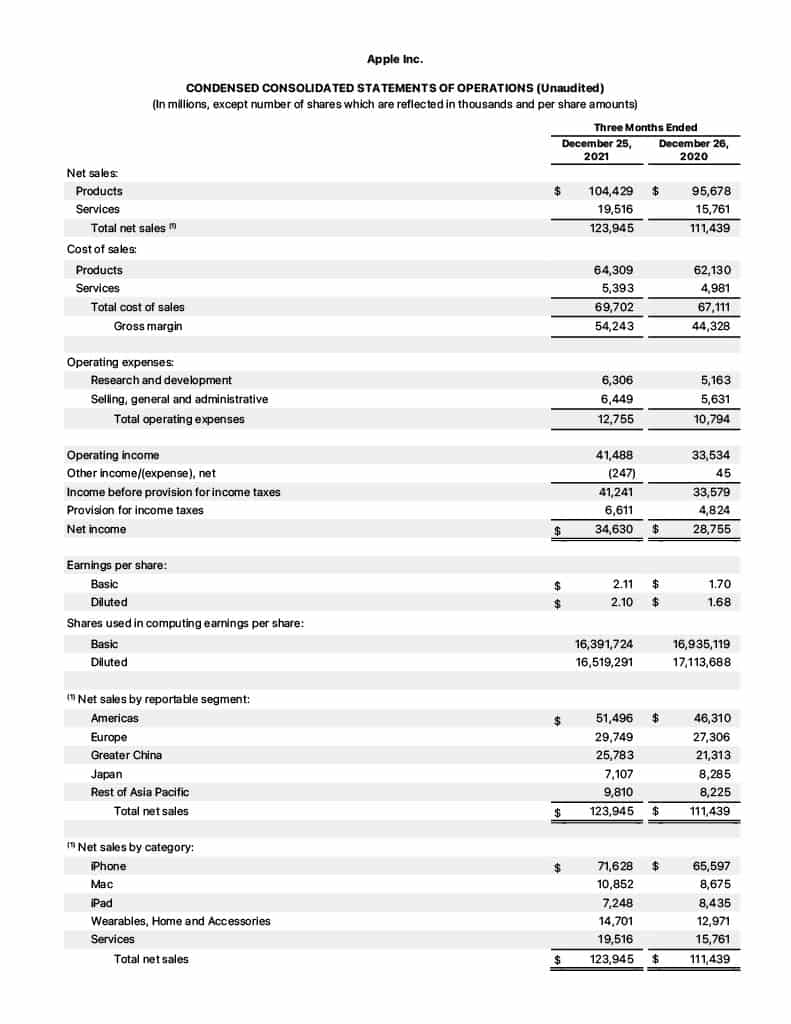

Here is an example of the multi-step Income Statement for Apple:

When is an Expense Recognized or Considered to be Incurred?

When an expense is recorded is based on the accounting method a company uses, cash basis or accrual basis. Under the Cash Basis method, an expense is only incurred (recorded on the Income Statement) when cash is paid out. Under the Accrual Basis method, an expense is recognized (recorded on the Income Statement) when the services are delivered or the goods are delivered, regardless of when cash is received.

For businesses required to follow U.S. Generally Accepted Accounting Principles (GAAP), the Accrual Basis of accounting is required.

For more information about GAAP, watch this video:

What is the Difference Cash Basis and Accrual Basis?

Under Cash Basis of accounting, revenue is considered to be earned (included in revenue on the income statement) when cash is received. Expenses are considered to be incurred (included in expenses on the income statement) when cash is paid out.

Under Accrual Basis of accounting, revenue is considered to be earned (included in revenue on the income statement) at the time the work is completed or the goods are delivered, regardless of when cash is received. Expenses are considered to be incurred (included in expenses on the income statement) when the services are received or goods are received, regardless of when cash is paid out.

For more information about Cash Basis vs Accrual Basis, watch this video:

What is the difference between Accrued Expense and Deferred Expense?

Accrued Expense represents expenses incurred but not yet paid for. An example of Accrued Expense is a purchase from a vendor on account. The expense is recorded in the current month and tracked using Accounts Payable. The portion of the expense incurred in the current month is included in expenses, but the cash will be paid out in a later month.

Deferred Expense represents payments made prior to the work being done or the goods being delivered. The cash payment is recorded to a deferred or prepaid revenue account (an Asset) until it is used up, at which time it will be moved from the asset account to the related expense account. An example of a deferred expense is Prepaid Insurance.

For more information about Prepaid Expenses, read this article:

Chart of Accounts Listing of Typical Expenses

For more information about expenses are recorded, check out this article:

-

How to Know What to Debit and What to Credit in Accounting

If you’re not used to speaking the language of accounting, understanding debits and credits can seem confusing at first. In this article, we will walk through step-by-step all the building

-

How to Analyze Accounting Transactions, Part One

The first four chapters of Financial Accounting or Principles of Accounting I contain the foundation for all accounting chapters and classes to come. It’s critical for accounting students to get

-

What is an Asset?

An Asset is a resource owned by a business. A resource may be a physical item such as cash, inventory, or a vehicle. Or a resource may be an intangible

-

What are Closing Entries in Accounting? | Accounting Student Guide

What is a Closing Entry? A closing entry is a journal entry made at the end of an accounting period to reset the balances of temporary accounts to zero and

-

What is a Liability?

A Liability is a financial obligation by a person or business to pay for goods or services at a later date than the date of purchase. An example of a

-

What is Revenue?

Revenue is the income generated by a business in the normal course of operations. It represents the sale of goods and services to customers or clients. For a non-profit organization,