In accounting, a Prepaid account represents cash expended prior to goods or services being received. Examples of Prepaid accounts are Prepaid Expense, Prepaid Rent, and Prepaid Insurance. A Prepaid account is an asset. It has a normal debit balance. It is listed in the Current Asset section on the Balance Sheet.

What are Some Examples of Prepaid Accounts?

This table shows a list of common prepaid accounts businesses use to track the amounts the business prepays for future goods and services.

| Prepaid Rent | Prepaid Insurance |

| Prepaid Subscriptions | Prepaid Interest |

| Prepaid Expenses | Prepaid Taxes |

What is Prepaid Rent?

Prepaid Rent represents rent paid to a landlord prior to when the rent is due. An example of prepaid rent would be a landlord requiring first and last month’s rent at the time the lease is signed. The first month’s rent would be recorded as Rent Expense while the last month’s rent would be recorded as Prepaid Rent. Prepaid Rent is an Asset. It has a normal debit balance. It increases on the debit side.

The journal entry for Prepaid Rent is:

| Prepaid Rent | 1200 | |

| Rent Expense | 1200 | |

| Cash | 2400 |

When the Prepaid Rent is “used up”, an adjusting journal entry is used to move the amount out of Prepaid Rent and into Rent Expense:

| Rent Expense | 1200 | |

| Prepaid Rent | 1200 |

If a business prepaid three months of rent, as each month passes, one month’s rent is moved from Prepaid Rent into Rent Expense. The original journal entry would be:

| Prepaid Rent | 3600 | |

| Cash | 3600 |

When the first month’s rent is due, an adjusting journal entry is done to move one month’s rent from Prepaid Rent to Rent Expense:

| Rent Expense | 1200 | |

| Prepaid Rent | 1200 |

After the first month’s journal entry is completed, the balance in Prepaid Rent is now $3,600 – $1,200 = $2,400.

When the second month’s rent is due, an adjusting journal entry is done to move one month’s rent from Prepaid Rent to Rent Expense:

| Rent Expense | 1200 | |

| Prepaid Rent | 1200 |

After the second month’s journal entry is completed, the balance in Prepaid Rent is now $3,600 – $2,400 = $1,200.

The final adjusting journal entry is done in the third month, bringing the balance in Prepaid Rent to zero.

What is Prepaid Insurance?

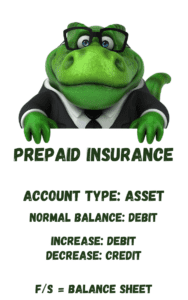

Prepaid Insurance represents insurance premiums paid to insurers in advance. An example of this is a company paying a year of insurance in advance. Prepaid Insurance is an Asset. It represents cash paid for services that have not yet been received. It has a normal debit balance. It increases on the debit side. It is listed in the Current Asset section on the Balance Sheet.

The journal entry for Prepaid Insurance is:

| Prepaid Insurance | 2400 | |

| Cash | 2400 |

As the Prepaid Insurance is “used up”, an adjusting journal entry is used to move the amount out of Prepaid Insurance and into Insurance Expense:

| Insurance Expense | 200 | |

| Prepaid Insurance | 200 |

This adjusting journal entry would be done each month for twelve months until the prepaid premium is “used up” and the balance is zero.

What is Prepaid Expenses?

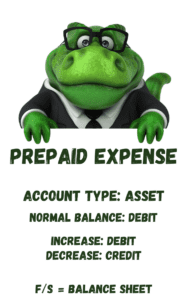

Prepaid Expenses is an account used to track the payment in advance of any substantial prepayments for goods and services. This could include goods paid for in advance of delivery or services paid for in advance of the service being delivered. Prepaid Expense is an Asset. It represents cash paid for services or goods in the current month that will be received in a future month. It has a normal debit balance. It increases on the debit side. It is listed in the Current Asset section on the Balance Sheet.

Prepaid Expense account is used to record amounts that are paid for in one accounting period and received in another accounting period. An example of a Prepaid Expense is prepaid marketing. If a company is required to pay in advance for marketing consulting on a contract that will be completed in the next month, Prepaid Expense is used to record the prepayment. When the contract is completed the next month, the amount is moved out of Prepaid Expense and into Marketing Expense using an adjusting journal entry.

Here is the original journal entry to record the prepayment of marketing costs:

| Prepaid Expense | 10,000 | |

| Cash | 10,000 |

Here is the adjusting entry in the next month to record the receipt of the services:

| Marketing Expense | 10,000 | |

| Prepaid Expense | 10,000 |

The balance in Prepaid Expense is now zero.

How are Prepaid Expenses are Listed on the Balance Sheet

On the Balance Sheet, Prepaid accounts including Prepaid Insurance, Prepaid Rent, and Prepaid Expenses are recorded in the Current Asset section.

On the Balance Sheet, the Prepaid accounts would be listed:

| Assets |

| Current Assets |

| Cash |

| Accounts Receivable |

| Prepaid Rent |

| Prepaid Insurance |

| Prepaid Expense |

For step-by-step guidance on how to do journal entries, check out this article:

-

How to Know What to Debit and What to Credit in Accounting

If you’re not used to speaking the language of accounting, understanding debits and credits can seem confusing at first. In this article, we will walk through step-by-step all the building

-

How to Analyze Accounting Transactions, Part One

The first four chapters of Financial Accounting or Principles of Accounting I contain the foundation for all accounting chapters and classes to come. It’s critical for accounting students to get

-

What is an Asset?

An Asset is a resource owned by a business. A resource may be a physical item such as cash, inventory, or a vehicle. Or a resource may be an intangible

-

Difference Between Depreciation, Depletion, Amortization

In this article we break down the differences between Depreciation, Amortization, and Depletion, discuss how each one is used, and what the journal entries are to record each. The main

-

What are Closing Entries in Accounting? | Accounting Student Guide

What is a Closing Entry? A closing entry is a journal entry made at the end of an accounting period to reset the balances of temporary accounts to zero and

-

What is a Liability?

A Liability is a financial obligation by a person or business to pay for goods or services at a later date than the date of purchase. An example of a