The Statement of Retained Earnings is one of the four major financial statements. The function of the Statement of Retained Earnings is to show changes in the value of equity in a corporation. It also serves as the link between the Income Statement and the Balance Sheet where profits and losses are passed from the Income Statement to the Balance Sheet equity accounts.

The Statement of Retained Earnings is also known as the Retained Earnings Statement, Statement of Shareholders’ Equity, Statement of Owner’s Equity, Statement of Partners’ Equity, Statement of Members Equity. The title of the report generally follows the ownership structure of the company.

- Corporations–Statement of Retained Earnings, Statement of Shareholders’ Equity

- Sole Proprietorships–Statement of Owner’s Equity

- Partnerships–Statement of Partners’ Equity

- Limited Liability Companies–Statement of Members’ Equity

In larger corporations, the Statement of Retained Earnings may be a section within the Statement of Shareholders’ Equity.

How is Retained Earnings Calculated?

The Statement of Retained Earnings reports on the changes that occur to equity during a specified amount of time (month, quarter, year). It starts with the beginning balance, adds net income, and subtracts dividends to arrive at the new ending balance.

Beginning Retained Earnings + Net Income – Dividends = Ending Retained Earnings

To understand the calculation, let’s break down the components.

What is Retained Earnings?

Retained Earnings is the cumulative amount of profits and losses for a business less any dividends paid to owners (sole proprietors, partners, members or shareholders).

What is Net Income?

Net Income is the difference between Revenues and Expenses. When Revenues are greater than Expenses, a company has Net Income (Profit). When Expenses are greater than Revenues, a company has a Net Loss (Loss). Net Income increases the value of an owner’s equity in a business. Net Loss decreases the value of an owner’s equity in a business.

For more information about Net Income, check out this article:

What are Dividends?

A dividend is a business distributing some or all of its earnings (profits minus losses) to its owners. For a sole proprietorship, this may be called a Dividend, Distribution, Owner’s Draw, or Owner’s Withdrawal. For corporations, it is generally referred to as a Dividend.

A dividend reduces the amount in Retained Earnings since it is the distribution of earnings. The corporation is taking money out of the business to give to owners (shareholders).

For additional information about accounting for Dividends, check out this article:

Statement of Retained Earnings Example

As an example, we’ll say Terrance Inc. had the following profits and losses for the years indicated:

| Terrance Inc. | 2024 | 2025 | 2026 |

| Net income/(loss) | 10,000 | (5,000) | 15,000 |

For the purposes of this example, we will assume Terrance Inc. began operations on January 1, 2024. When a business is new, the beginning balance for all accounts is zero.

Ignoring any Dividends for the moment, the Statement of Retained Earnings for Terrance Inc. on December 31, 2024 shows an Ending Retained Earnings balance of $10,000.

Beginning Retained Earnings + Net Income – Dividends = Ending Retained Earnings

Statement of Retained Earnings for 2024

| Beginning Retained Earnings, Jan. 1, 2024 | 0 |

| Net Income | 10,000 |

| Dividends | (0) |

| Ending Retained Earnings Dec. 31, 2024 | 10,000 |

The Ending Retained Earnings balance for Dec. 31, 2024 is the new Beginning Retained Earnings balance for 2025.

Ignoring any Dividends for the moment, the Statement of Retained Earnings for Terrance Inc. on December 31, 2025 shows an Ending Retained Earnings balance of $5,000.

Statement of Retained Earnings for 2025

| Beginning Retained Earnings, Jan. 1, 2025 | 10,000 |

| Net Income | (5,000) |

| Dividends | (0) |

| Ending Retained Earnings Dec. 31, 2025 | 5,000 |

Ignoring any Dividends for the moment, the Statement of Retained Earnings for Terrance Inc. on December 31, 2026 shows an Ending Retained Earnings balance of $5,000.

Statement of Retained Earnings for 2026

| Beginning Retained Earnings, Jan. 1, 2026 | 5,000 |

| Net Income | 15,000 |

| Dividends | (0) |

| Ending Retained Earnings Dec. 31, 2026 | 20,000 |

Now, let’s look at what happens when Terrance Inc. pays dividends.

| Terrance Inc. | 2024 | 2025 | 2026 |

| Net income/(loss) | 10,000 | (5,000) | 15,000 |

| Dividends | 2,000 | 1,000 | 5,000 |

Statement of Retained Earnings for 2024

| Beginning Retained Earnings, Jan. 1, 2024 | 0 |

| Net Income | 10,000 |

| Dividends | (2,000) |

| Ending Retained Earnings Dec. 31, 2024 | 8,000 |

Statement of Retained Earnings for 2025

| Beginning Retained Earnings, Jan. 1, 2025 | 8,000 |

| Net Income | (5,000) |

| Dividends | (1,000) |

| Ending Retained Earnings Dec. 31, 2025 | 6,000 |

Statement of Retained Earnings for 2026

| Beginning Retained Earnings, Jan. 1, 2026 | 6,000 |

| Net Income | 15,000 |

| Dividends | (5,000) |

| Ending Retained Earnings Dec. 31, 2026 | 16,000 |

How to Prepare a Statement of Retained Earnings

- Determine time period to be covered. The statement is generally prepared monthly, quarterly, or yearly.

- Begin with the ending balance in Retained Earnings from the previous period. For a new business, the balance is zero. For an existing business, the balance is the total of all Profits and Losses minus any dividends paid out.

- Add Net Income (or subtract Net Loss) for the total period covered by the statement being prepared. This number comes from the Income Statement (Profit & Loss Statement) for the company.

- Subtract Dividends paid to the owners or shareholders during the period of time the statement covers. This number comes from the activity in the Dividends account in the Chart of Accounts.

- The remaining balance is the ending balance in the Retained Earnings account.

- As with all financial statements, the heading of the report shows the name of the company, the name of the report, and the period of time the report is based on (month, quarter, year).

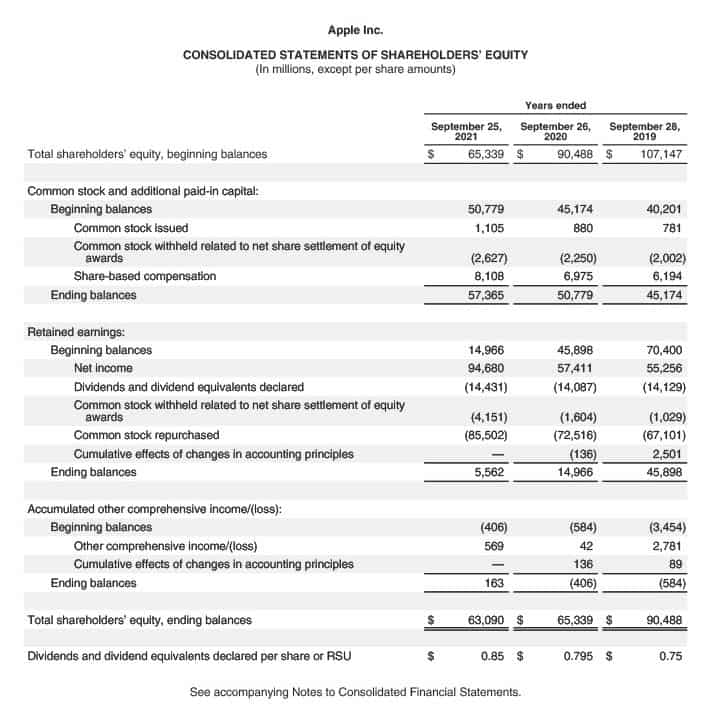

Statement of Retained Earnings for Apple Inc.

In the example report below, focus on the Retained Earnings section. It starts with the beginning balance, adds net income, and subtracts dividends. The other items included are specific to the company. One item to note is the “Common stock repurchased” line. The company has used a large portion of its earnings to buy back its own stock (Treasury Stock.)

For more information about accounting for Treasury Stock, check out this article:

What Does the Statement of Retained Earnings Show?

The job of the Statement of Retained Earnings is to tracks changes in the equity for all owners. It indicates how a corporation is choosing to use its earnings.

Is it distributing the excess earnings to shareholders as dividends or is it holding on to earnings to finance large projects or initiatives? Is it using the the earnings to buy back its own stock in the form of Treasury Stock?

Like all financial statements, the Statement of Retained Earnings gives one view of the finances of a business. When the Income Statement, Statement of Retained Earnings, Balance Sheet, and Statement of Cash Flow are examined separately and as a whole, a picture of the overall health and decisions of the company can come into focus.

For more information and examples about the Statement of Retained Earnings/Owner’s Equity/Shareholders Equity report, watch this video:

For access to the example spreadsheet in the video, click this Google Drive link: Statement of Owner’s Equity Examples