What is Stock in a Corporation?

Stock represents shares of ownership in a corporation. Each share of stock represents one share or fraction of ownership in the corporation. Publicly traded corporations issue stock in an Initial Public Offering (IPO). Once issued in an IPO, the stock can then be traded (bought and sold) between investors on the stock market.

What is a Publicly Traded Corporation?

A publicly traded or publicly held corporation is one where the corporation’s stocks are available for purchase by the public on the stock market. A privately held corporation does not offer or trade its stock to the public. A privately held corporation’s stock is owned by the founders, managers, or private investors.

Why Do Corporations Issue Stock?

Corporations issue (sell) stock to investors to raise capital to expand the business or take on large new projects. Through the sale of stocks, corporations trade partial ownership (equity) in the corporation for cash. When stocks are issued, they are generally assigned a type of either Common Stock or Preferred Stock.

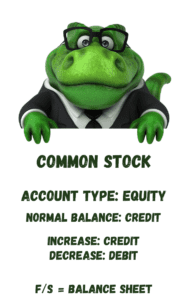

What is Common Stock?

Common Stock is the most “common” stock issued by a corporation. Each share of Common Stock represents a fraction (share) of ownership in the company. Common Stock holders have the right to vote to elect the corporation’s board of directors and to vote on corporate policies. Common Stock holders only receive dividends once Preferred Stock holders have received all required dividends. In accounting, Common Stock is also the name of the account used to track the issuance (sale) of Common Stocks. Common Stock is an equity account. Common Stock has a normal credit balance. It increases on the credit side and decreases on the debit side. Common Stock is listed in the equity section of the Balance Sheet.

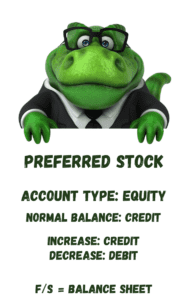

What is Preferred Stock?

Preferred Stock is a special type of stock issued by a corporation. Like Common Stock, each share of Preferred Stock represents a fraction (share) of ownership in the company. Unlike Common Stock, Preferred Stock holders do not have the right to vote to elect the corporation’s board of directors and to vote on corporate policies. Preferred Stock holders receive preferential treatment when it comes to dividends. Preferred Stock pays regular dividends that may provide more predictable income to investors. In accounting, Preferred Stock is also the name of the account used to track the issuance (sale) of Preferred Stocks. Preferred Stock is an equity account. Preferred Stock has a normal credit balance. It increases on the credit side and decreases on the debit side. Preferred Stock is listed in the equity section of the Balance Sheet.

For more information about the differences between Preferred Stock and Common Stock, watch this video:

How Are Stock Prices Determined?

When a corporation initially issues stock in an Initial Public Offering (IPO), the stock is assigned a value based on an analysis of the stock’s worth by investment bankers. Investors purchase the new stock. The demand for the stock drives the price during the IPO. Once the stock is available for resale by investors, the price is driven by supply and demand. Corporations can offer stock at par, without par, at a premium, or at a discount.

What is Par Value?

When it comes to stocks, par value is the stated value assigned to a stock by the corporation when the stock is issued. It’s usually a very small amount. It represents the absolute least price a stock can sell for. It may be a penny or a dime or a dollar.

What is Premium on Stock?

What a stock sells at more than par value, the stock is sold at a premium. The value received for the stock in higher than the par value. The value of the amount above par is recorded in an account called Paid-in Capital or Paid-in Capital in Excess of Par. Paid-in Capital is an equity account. It has a normal credit balance. Paid-in Capital increases on the credit side and decreases on the debit side.

What is Discount on Stock?

When a stock sells at less than par value, the stock is sold at a discount. The value received for the stock is less than the par value. The value of the amount below par is recorded in an account called Discount on Issue of Share. This is rare. Discount on Issue of Share is a contra equity account. A contra equity account has a normal debit balance. Discount on Issue of Share increases on the debit side and decreases on the credit side.

Accounting Transactions for Issuance of Common Stock

Issuance of No-Par Common Stock

A corporation issued 1,000 shares of no-par common stock. The stock was issued at $30.

| Cash | 30,000 | |

| Common Stock (1,000 shares of no-par common stock at $30) | 30,000 |

Issuance of Common Stock at Par

A corporation issued 1,000 shares of common stock with a $30 par.

| Cash | 30,000 | |

| Common Stock (1,000 shares of $1 par common stock at $30) | 30,000 |

Issuance of Common Stock at Premium

A corporation issued 1,000 shares of common stock with a $1 par. The stock was issued at $35 including a premium of $5.

| Cash | 35,000 | |

| Common Stock (1,000 shares of $1 par common stock at $30) | 1,000 | |

| Additional Paid-in Capital (1,000 shares of $1 par common stock at $30) | 34,000 |

Issuance of Common Stock at Discount

A corporation issued 1,000 shares of common stock with a $30 par. The stock was issued at $25 including a discount of $5.

| Cash | 25,000 | |

| Discount on Issue of Share | 5,000 | |

| Common Stock (1,000 shares of $1 par common stock at $25) | 30,000 |

Accounting Transactions for Issuance of Preferred Stock

Issuance of No-Par Preferred Stock

A corporation issued 1,000 shares of no-par preferred stock. The stock was issued at $30.

| Cash | 30,000 | |

| Preferred Stock (1,000 shares of no-par preferred stock at $30) | 30,000 |

Issuance of Preferred Stock at Par

A corporation issued 1,000 shares of preferred stock with a $30 par.

| Cash | 30,000 | |

| Preferred Stock (1,000 shares of $1 par preferred stock at $30) | 30,000 |

Issuance of Preferred Stock at Premium

A corporation issued 1,000 shares of preferred stock with a $1 par. The stock was issued at $35 including a premium of $5.

| Cash | 35,000 | |

| Common Stock (1,000 shares of $1 par preferred stock at $30) | 1,000 | |

| Additional Paid-in Capital (1,000 shares of $1 par preferred stock at $30) | 34,000 |

Issuance of Preferred Stock at Discount

A corporation issued 1,000 shares of preferred stock with a $30 par. The stock was issued at $25 including a discount of $5.

| Cash | 25,000 | |

| Discount on Issue of Share | 5,000 | |

| Common Stock (1,000 shares of $1 par preferred stock at $25) | 30,000 |

Recording stock transactions in accounting carries with it a level of complexity that lies outside the context of this article. These sample stock journal entries are not a definitive guide to journal entries related to stock transactions. They are meant as an overview for accounting students to offer a sampling of basic journal entries relating to stock transactions.

What Financial Statements Show Stockholder’s Equity?

Details about Stockholder’s Equity are reported on the Statement of Stockholders’ Equity and summarized on the Balance Sheet.

To learn more about how stockholders’ equity is reported on the Statement of Stockholders’ Equity, watch this video:

To learn more about how stockholders’ equity is reported on the Balance Sheet, watch this video:

Related Articles:

-

What is Equity in Accounting and Finance?

In Accounting and Finance, Equity represents the value of the shareholders’ or business owner’s stake in the business. Equity accounts have a normal credit balance. Equity increases on the credit

-

What is Treasury Stock?

Treasury Stock represents a corporation’s stocks that were previously issued and sold to shareholders. The corporation reacquires the stock by purchasing the stock from shareholders. Treasury Stock reduces the number

-

What is Stockholders’ Equity?

Stockholders’ Equity is the difference between what a corporation owns (Assets) and what a corporation owes (Liabilities). Stockholders’ Equity is made up of Contributed Capital and Earned Capital. Contributed Capital

-

What is Paid in Capital?

What is Contributed or Paid-in Capital? Contributed Capital is also called Paid-in Capital. It includes any amounts “contributed” or “paid in” by investors or stockholders through purchasing of stocks or

-

What are Dividends? | Accounting Student Guide

What is a Dividend? A Dividend is a payout of earnings by a corporation to its stockholders. Dividends can be cash dividends or stock dividends. A dividend is paid per

-

What are Stock Splits?

A stock split occurs when a corporation’s board of directors decides to divide one share of stock into multiple shares. For example, a two-for-one stock split means that one share